[Week 21 of 2026] SpaceX, SpaceX, and SpaceX

![[Week 21 of 2026] SpaceX, SpaceX, and SpaceX](https://storage.ghost.io/c/30/e9/30e9cd1a-3aaa-4254-8a97-d884d5cdb64c/content/images/size/w960/2026/05/week-2026-21.png)

Welcome back to Price and Prejudice with a few musings from Week 21 of 2026.

SpaceX Galore – Part 1

Perhaps the biggest news in capital markets this week is SpaceX's S-1 filing, which is the initial registration statement required by the SEC before IPO. Skimming the S-1 is a fun exercise because it reveals so much about the underlying company that we previously knew so little about.

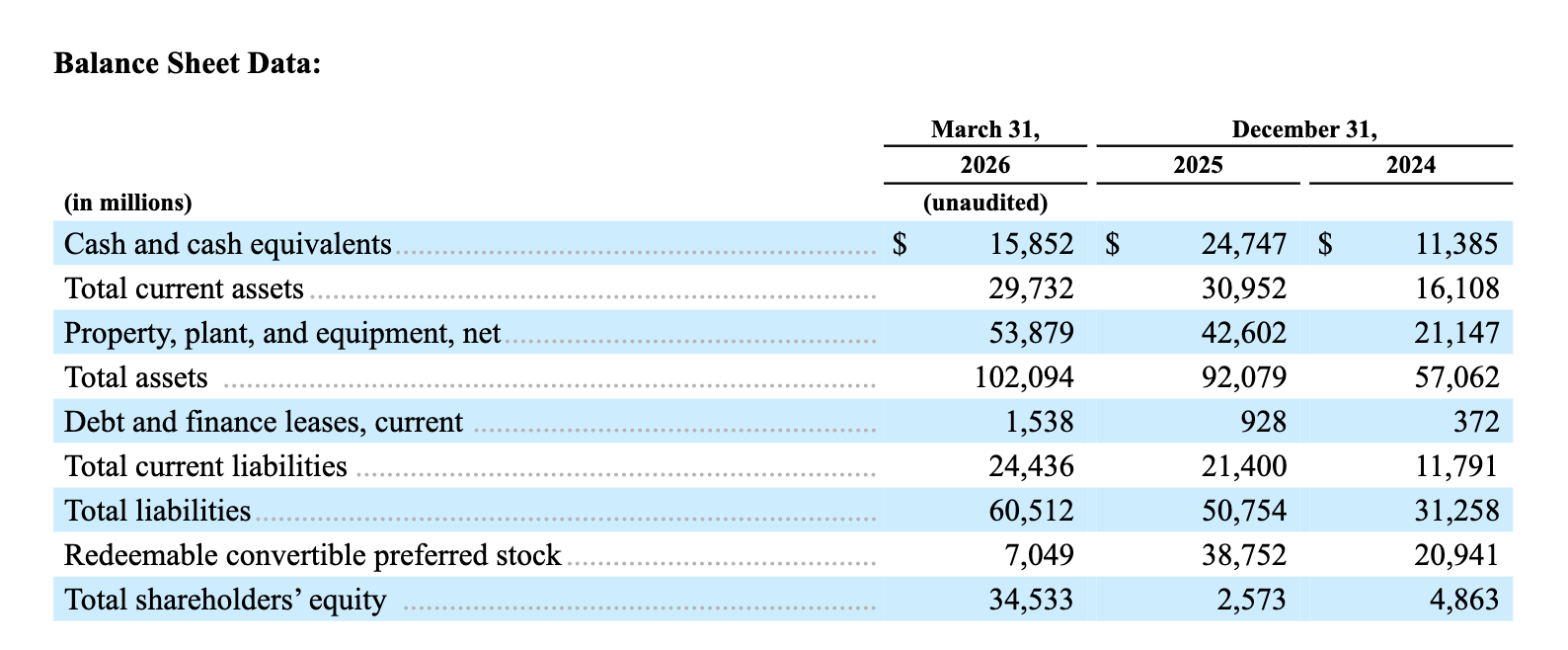

Here's one snippet on governance:

which somewhat confirms what the market already suspected: Musk walks into the public market with 85.1% of the voting power despite owning a much smaller share of the economic claim. This is because Class B shares carry 10 votes each, and Class B is the only class that can remove Musk from CEO, chairman, or the board. As this article points out, Musk can only be fired if he votes against himself.

How unusual is this situation? Dual-class IPOs are nothing new (Google, Snap, Meta), but the trajectory has been toward more founder control at larger scale, not less. This is also part of a broader trajectory where someone who wants the residual claim on the company's profits may not necessarily want the voting power. Still for the median listed firm, voting rights and board accountability are part of what makes the share a residual claim worth holding. For SpaceX, the residual claim is a bet on a person, and the pricing of that bet is pretty much the entire story.

SpaceX Galore – Part 2

There are many reasons why companies go public. Given the size of this particular IPO, the natural reading is (i) founder liquidity plus (ii) capital for growth.

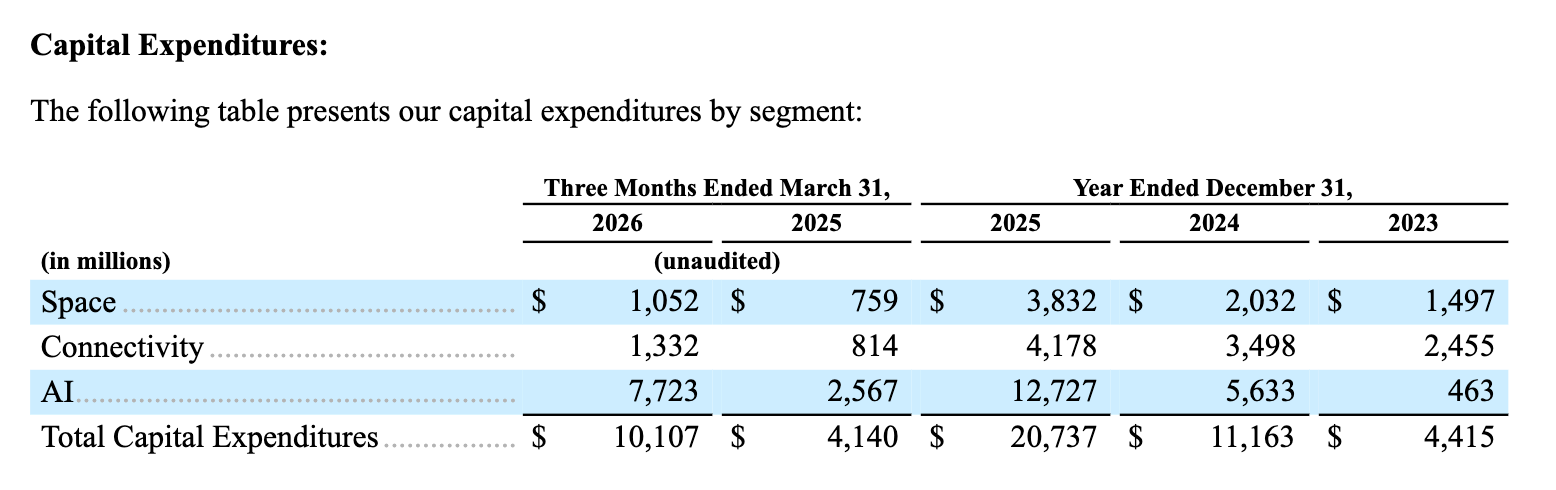

The filings, however, tell a slightly different story. For example, cash holdings fell from $24.7 billion to $15.9 billion in a single quarter:

and AI capex was $7.7 billion in Q1 2026 alone (vs. $1.1 billion for Space capex):

which seems to suggest that most of the IPO money will likely fund this ongoing burn. This in fact makes it closer to a late-stage venture where multi-year operating losses are covered while the the underlying businesses scale. In some sense, even with the IPO, this look awfully like a private capital markets deal.

Perhaps, the more useful way to think about this is that the public-private boundary has been collapsing in both directions: private companies stay private longer and raise public-equivalent rounds in late-stage venture; public companies, when they finally list, do so at sizes that resemble late-stage venture.

SpaceX Galore – Part 3

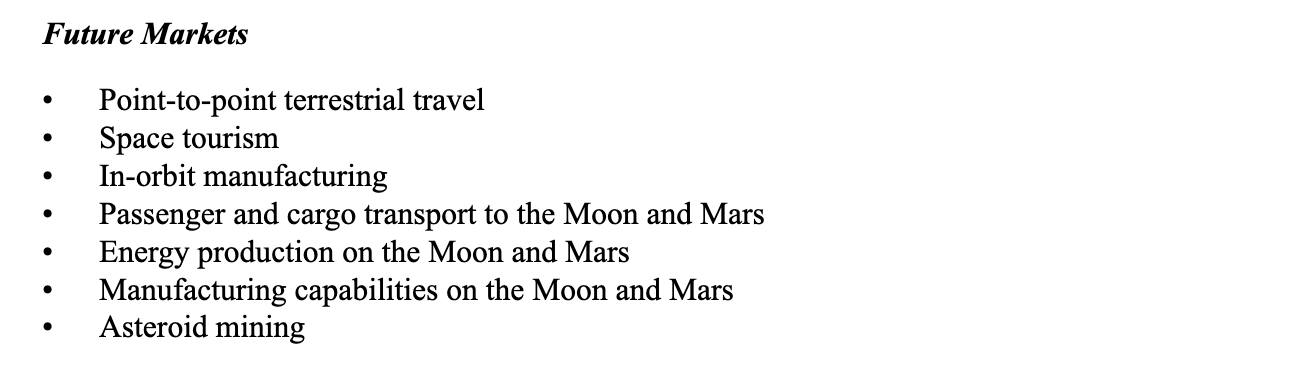

Another fun part about S-1 is that they often come up with company-specific metrics that are hard to port elsewhere. One thing that stands out is the $28.5 trillion total addressable market, of which 93% is AI:

with a pretty cool list of future markets:

which comes with its unique challenges:

It is genuinely impressive prose for a securities filing, but as a market-sizing exercise is a bit hard to swallow since (i) the cited sub-markets do not exist as commercial activities, and (ii) the ones that do (launch, broadband) make up a small fraction of the $28.5 trillion number.

The more charitable reading is that the TAM section is doing disclosure work the financial statements cannot. Effectively, the TAM list functions as a catalogue of the long-dated real options the firm is choosing to keep alive. The dollar figure attached to that list is probably noise, but the composition of the list is real disclosure. And for investors trying to underwrite a company whose value is largely in long-dated optionality, the catalogue of what management is willing to plant a flag in might still be useful.